Employee benefits have become a key part of the hiring and retention of employees in today’s hiring market. There is more stress on compensation now more than ever as demand for higher salaries and pay rates comes equally from potential hires as it does from the existing workforce.

An employer’s willingness to put the time and effort into their employees benefits outside of wages may make the difference. At a high level, total compensation and employee benefits includes, but is not limited to, health insurance, wellness programs, life insurance and retirement or defined benefit plans.

Health Insurance

More specifically, health insurance can provide employees compensation in the form of reducing out of pocket exposure when it comes to their healthcare needs and access to their providers.

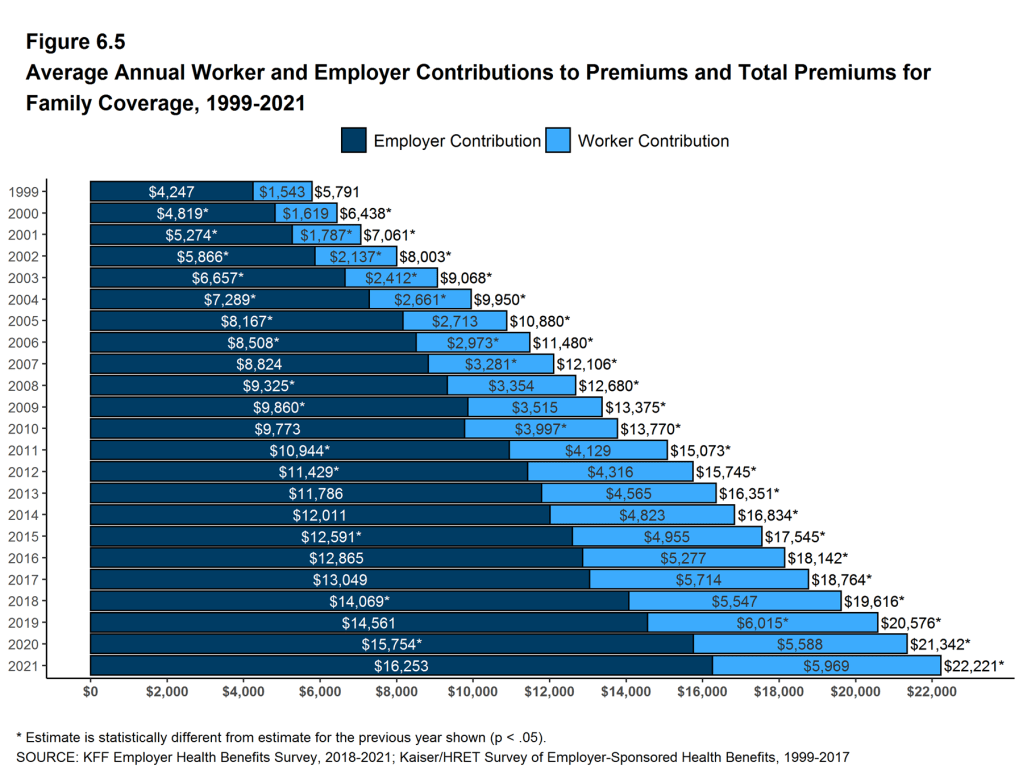

Health insurance typically accounts for one of the largest P&L expenses for an employer outside of payroll. Typically there is a cost share for this expense (the insurance premium) between the employees and the employer. Benchmark data from the Kaiser Family Foundation (KFF) stated that in 2020 the average employer share of this expense fell between 60-70%, leaving the employees with ~30%-40% of the premium responsibility deducted out of their payroll. 2021 KFF findings here: https://www.kff.org/health-costs/. Companies could argue that they are essentially compensating their employees by covering a larger percentage of their healthcare premium on top of what they pay them through payroll.

However, these figures have shifted somewhat throughout the pandemic. As companies have found it more difficult to create higher payroll some have decided to take on more of the premium burden, leaving their employees with more of their payroll to spend on other things such as living expenses. However, as we have come out on the other side of the pandemic (somewhat), health insurance premiums have gone up significantly – raising more than 7% on average year-over-year from 2021-2022 which renewal increases reaching 30-40% in some cases that we’ve seen. This has created cost share shift in the opposite direction, resulting in employers deducting more out of payroll to accommodate the increases.

These renewal increases our driven by a couple primary factors. The first is that during the pandemic, many “non-essential” procedures (or non-emergency procedures) were delayed as providers did not have the capacity to perform such procedures during the height of COVID-19. The result was that claims for companies went down substantially therefore smaller premium increases were given by health insurance underwriters during the 2021 renewal season. However, going into 2022, underwriters took on a much more conservative outlook – knowing that claims would rebound and increase as many procedures users could not do in the previous year would occur during this year.

The receipt of such unfavorable increases has driven companies to reconsider the plans they provide their employees. PPO plans offer broader network, copays for doctor’s visits (primary care) as well as specialists covered under the network and prescriptions. HSA plans are high deductible health plans (HDHP: exceeding $1,400 for individual deductible and $2,800 in family deductible) and require the user to cover the deductible expense out of pocket before the plan contributes to the healthcare expenses at a coinsurance. PPO plans typically charge higher premiums but require less out of pocket expenses because of their copay structure. HSA plans typically charge less premium but require more up front out of pocket expense to reach the deducitble limit. Additionally, they offer the user a tax-free way to put aside money for qualified medical expenses, defined by the plan.

When faced with such material increases, companies look to transition to plans with cheaper premiums – i.e. higher deductibles, more narrow networks, etc. to migrate their employees to plans that may create a lesser expense for the company. However, employers often overlook the headache that such a change may cause for their employees. For instance, if you are an employee used to paying a $30 copay for a doctor’s visit under a PPO plan, but now has to foot the entirety of the doctor’s visit bill until you reach your deductible under an HSA plan – that may cause some stress. Further, if an employer moves to a narrower (smaller) network to reduce premium which causes a major local hospital system to be considered out-of-network and not covered by the plan, and HR director will be facing some tough conversations with employees.

These changes, which seem like the right thing to do on the surface, cause more employees to seek other places of employment. Even more so than higher wages. This is why the decisions must be carefully made and analyzed before finalized. The use of an experienced insurance broker will help do just that.

Many HR professionals have experience with their own population of employees, payroll and benefits at some level. However, the broadness of experience dealing with different health insurance carriers, networks, plans, benchmarks, etc. requires the use of an objective third-party with a breadth of employee benefits knowledge.

For over 130-years Oswald has done just that, provided expertise in the areas of health insurance/employee benefits, commercial P&C insurance, life insurance and retirement plans to our clients. We work with our clients to make informed decisions that can be tough at times – but are backed by data, analysis and market information. We serve over 2,000 clients nationally and are among the largest privately held, employee-owned and independent brokerages in the country.

By partnering with a broker such as Oswald, not only is the company getting the advice that they need to make decisions at the leadership level, but employees are also getting the assistance they need from a service team to enroll in the right plan.

Brian Stovsky is Business Development Leader, Private Equity, Oswald Companies